The P2P database illustrates the ability of a wide range of occupations to afford typical housing in metropolitan areas across the country.

NHC’s Paycheck to Paycheck database illustrates the ability – or lack thereof – of working families to afford typical housing in metropolitan areas across the country by comparing wage data and housing costs.

We update our database every quarter to keep up with the country’s rapidly changing housing market. In conjunction with these updates, we issue quarterly reports highlighting a different angle of the housing costs facing families across the country. Check out our visualization tool below or download the data yourself to get the latest snapshot of housing affordability across the country.

“Priced Out: When a good job isn’t enough”

(September 2025)

The U.S. housing market is facing a nationwide affordability crisis that now impacts workers across nearly all income levels. Decades of underbuilding, rising interest rates, and wage stagnation have combined to push both homeownership and rental housing further out of reach. This report from NHC uses its Paycheck to Paycheck database to track affordability changes in 390 metropolitan statistical areas (MSAs) from 2019 to 2024, with focused case studies in Asheville, Boise City, Houston, Tampa, and Seattle.

Key Findings

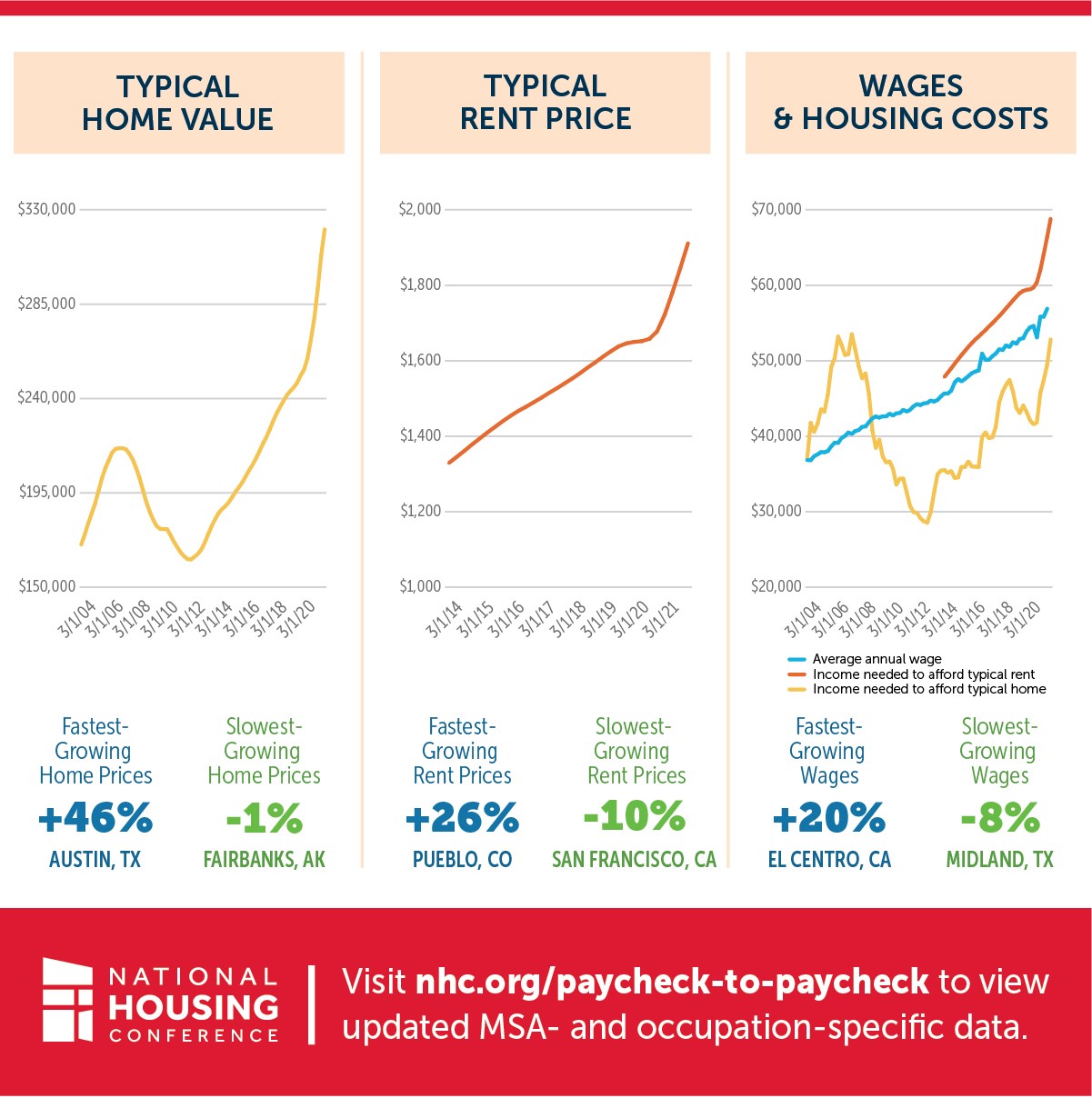

- Homeownership Costs Have Surged: In 2024, 176 MSAs require a six-figure income to buy a typically priced home with 10% down, up from 30 in 2019. In 125 MSAs, the income needed to purchase has at least doubled since 2019.

- Renting Is Increasingly Unaffordable: Nearly half (47%) of tracked occupations cannot afford a two-bedroom apartment, compared to 38% in 2019. In 32 MSAs, the salary needed to comfortably rent exceeds $75,000.

- Wages Lag Far Behind Costs: Even traditionally high-earning professionals are losing housing access. In Seattle, dentists cannot afford to buy a typically priced home; in Asheville, civil engineers are priced out despite earning nearly $100,000.

Paycheck to Paycheck uses three data sources:

- The Bureau of Labor Statistics’ (BLS) Metropolitan Area Occupational Employment and Wage Estimates gives median wage data for several hundred occupations disaggregated by metropolitan area.

- The Zillow Home Value Index gives typical home values for each metropolitan area.

- The Department of Housing and Urban Development’s (HUD) Fair Market Rent metric estimates the 40th percentile gross rent in each metropolitan area.

Using these three sources, we estimate the annual salary needed to afford to sustainably own or rent a home in 390 metropolitan areas, and compare that to the median annual salary for 150 occupations. (Due to regional differences in employment levels, BLS does not provide wage data for certain occupations in certain metropolitan areas. We are unable to compare wage and housing price data for those occupations in those areas.) We assume that rent should represent no more than 30% of one’s gross income, and that costs associated with homeownership should represent no more than 28% of one’s gross income (given the need to be able to pay for unforeseen maintenance costs).

When calculating the salary necessary to afford homeownership in a given metropolitan area, we assume the prevailing annual percentage rate (APR), property taxes equal to 1.1% of the value of the home annually, homeowner’s insurance equal to 0.35% of the value of the home annually, and private mortgage insurance equal to 1% of the value of the home annually.

Our affordability calculations are based on monthly housing costs, principally rent and mortgage payments. They do not account for other barriers to obtaining housing, such as saving up for a down payment, exclusionary zoning that renders neighborhoods near jobs and transit prohibitively expensive, or discrimination.

Job loss, housing composition changes, and personal preferences mean that many households rely on just one income to get by. In recent years, about a third of households in the United States had just one wage earner, and the median number of earners per household is around 1.3.

Reports & Data

{kind=link}

Sponsored By