WASHINGTON – “The administration’s changes to the False Claims Act are an important step towards reversing a decade of unintended consequences that have forced many of the nation’s best capitalized and most regulated financial institutions out of the FHA market,” said David M. Dworkin, NHC president and CEO. “A law that was meant to protect Civil War troops from lame mules and shoddy uniforms has no place in the mortgage finance system. Our regulations must protect consumers from bad mortgages, not from getting a mortgage.”

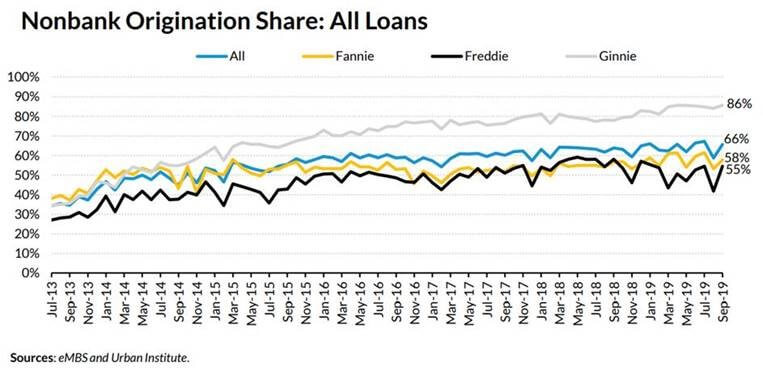

False Claims Act (FCA) settlements “wiped out a decade of FHA profitability,” JP Morgan Chase’s Jamie Dimon said. In his 2015 letter to shareholders, Dimon said that the bank drastically cut its FHA lending in 2015 due to the risk of a FCA charge from the government, among other factors. Between 2009 and 2016, when the Justice Department began using the False Claims Act in mortgage fraud cases, banks have agreed to over $7 billion in FCA settlements from lenders. By comparison, military procurement fraud settlements amounted to only $3.6 billion. The last FCA settlement with Quicken Loans resulted in a $32 million settlement for 109 “defective” loans. According to Urban Institute, from 2013 to 2019, nonbank share of government loan originations (FHA, VA, USDA loans) grew from less than 35% to 86% today. The False Claims Act (FCA), 31 U.S.C. §§ 3729 – 3733, was enacted in 1863 in response to defense contractor fraud during the American Civil War when defense contractors falsely sold lame mules and shoddy uniforms to the Union Army.

The National Housing Conference has been defending our American Home since 1931. #OurAmericanHome @natlhousingconf @davidmdworkin

About NHC: The National Housing Conference has been defending the American Home since 1931. Everyone in America should have equal opportunity to live in a quality, affordable home in a thriving community. NHC convenes and collaborates with our diverse membership and the broader housing and community development sectors to advance our policy, research and communications initiatives to effect positive change at the federal, state and local levels. Politically diverse and nonpartisan, NHC is a 501(c)3 nonprofit organization.

###