In light of COVID-19, we are temporarily making our Member Brief available to non-members. If you wish to become an NHC member, click here.

|

|

Weekly update from the National Housing Conference |

|

In this issue

February 14, 2021

Issue 90-6

• Members of Congress and housing groups support homeowner assistance

• HUD announces several fair housing actions

• Freddie Mac announces new equitable housing leadership positions

• FHFA extends COVID-19 protections and policies

• CFPB will prioritize consumer complaints

• Chart of the week: COVID-19 continues to have a disparate impact on minority households

|

Find the information you need at NHC's COVID-19 Housing Resource Center |

|

CRA and the intersection of geography and race

by David M. Dworkin, NHC President & CEO

Many of NHC’s members remain hard at work on their comment letters in response to the Federal Reserve Board’s Advance Notice of Proposed Rulemaking (ANPR) on the Community Reinvestment Act (CRA), which is due on Feb. 16. One of the most interesting and groundbreaking of the nearly 100 questions posed by the Fed is Question 2: “In considering how the CRA's history and purpose relate to the nation's current challenges, what modifications and approaches would strengthen CRA regulatory implementation in addressing ongoing systemic inequity in credit access for minority individuals and communities?” It seems like a fairly anodyne question, but despite the CRA being written to address the impact of redlining, race has never been a direct part of a CRA examination. Instead, proxies for race, like low- and moderate-income households and census tracts have been relied upon, while “community” has been defined strictly in geographic terms. Now the Fed is asking how, after 44 years, do we address the foundation of CRA – racial equity.

CRA stands at the intersection of geography and race. When enacted in 1977, the CRA responded to concerns over disinvestment in low-income communities and the persistent impact of “redlining,” the practice of avoiding investment in minority neighborhoods codified by the Home Owners' Loan Corporation (HOLC) in 1933 and the Federal Housing Administration in 1934. While the Fair Housing Act of 1968 prohibited redlining and other forms of housing discrimination, these practices proved difficult to reverse. Its impact has left deep scars in communities that persist more than a half century since the practice was outlawed. Research by economists at the Federal Reserve Bank of Chicago as recently as 2018 demonstrates that areas denied credit in the aftermath of the Great Depression continue to have lower property values, homeownership rates, and credit scores nearly 90 years later.

Non-White households’ access to affordable home mortgage loans today falls far short of what community advocates and legislative champions originally envisioned. Overall, Black homeownership plummeted during the Great Recession, falling from 49.7% in Q2 2004 to 40.6% in Q2 2019, when it was lower than it was when the Fair Housing Act was passed in 1968. This is a national tragedy. And Black and Hispanic households who have managed to become homeowners pay higher mortgage rates than their White counterparts and are at much greater risk of losing their homes during the pandemic.

|

|

Members of Congress and housing groups support homeowner assistance

“Across the nation people are struggling to make ends meet, and hunger is growing,” said House Financial Services Committee Chairwoman Maxine Waters (D-Calif.) during her opening statement. “Communities of color continue to be the hardest hit. The nation needs the $1.9 trillion in relief the American Rescue Plan would provide.” The committee also considered $10 billion in funding for struggling homeowners.

NHC helped lead more than 350 housing and civil rights organizations in a letter to congressional leaders advocating for additional funding for homeowners. The letter calls for $25 billion in direct assistance to homeowners facing hardships as a result of COVID-19, who disproportionately represent communities of color, with state housing finance agencies deploying the bulk of the funds through the Homeowner Assistance Fund. The letter also calls for at least $100 million for housing counseling and $39.7 million for the Fair Housing Initiatives Program.

Last week, Sens. Sherrod Brown (D-Ohio), Jack Reed (D-R.I.) and Patrick Leahy (D-Vt.) reintroduced the Homeowner Assistance Fund bill. “Millions of homeowners have fallen behind on their mortgages because of this pandemic, and the burden has fallen most heavily on families of color who have been disproportionately harmed during this crisis,” said Sen. Brown. “The Homeowner Assistance Fund will provide vital resources to keep families safe in their homes during and after this pandemic and keep us from deepening the inequities in our housing system.” |

|

|

HUD announces several fair housing actions

“We are pleased that HUD dropped its appeal,” said Jesse Van Tol, CEO of the National Community Reinvestment Coalition. “Now HUD and the Biden Administration can get to work driving discrimination out of housing. That should include fully rescinding HUD’s weakened disparate impact standard issued in 2020 and making it clear that HUD’s 2013 Disparate Impact Rule applies and will be followed.”

“Housing discrimination on the basis of sexual orientation and gender identity demands urgent enforcement action,” said FHEO Acting Assistant Secretary Jeanine M. Worden. “That is why HUD, under the Biden Administration, will fully enforce the Fair Housing Act to prohibit discrimination on the basis of gender identity or sexual orientation. Every person should be able to secure a roof over their head free from discrimination, and the action we are taking today will move us closer to that goal.”

|

|

|

|

Freddie Mac announces new equitable housing leadership positions

Freddie Mac announced the creation of two new leadership roles to address persistent housing disparity challenges in the single-family and multifamily markets. The GSE tapped Pamela Perry, a fair housing and community development expert, to serve as the vice president of single-family equitable housing. According to Freddie Mac, “Perry will lead a newly formed team responsible for creating solutions to break through historical barriers to achieving homeownership for minority families across the income spectrum, which has direct implications for wealth accumulation.”

“With this new position we are bringing a dedicated and distinct focus to address some of the most systemic issues we face in homeownership and wealth in communities of color, ” said Donna Corley, Freddie Mac executive vice president and head of single-family business.

Amanda Nunnink will serve as Perry’s counterpart on the multifamily side as vice president of equity in multifamily housing. Nunnink has worked in Freddie Mac’s multifamily business for nearly a decade and will work to “create sustainable improvements for renters and the rental housing industry,” while advancing diversity, equity and inclusion throughout the multifamily division.

“At Freddie Mac, we are taking active steps to embed diversity, equity and inclusion in every corner of our business,” said Debby Jenkins, Freddie Mac executive vice president and head of multifamily business.

|

|

|

|

|

FHFA extends COVID-19 protections and policies

The Federal Housing Finance Agency (FHFA) announced the extension of several policies and programs aimed at curbing the effects of the pandemic on households, lenders and mortgage servicers. Temporary loan flexibilities, originally set to expire on Feb. 28, will be extended through March 31. The temporary policies include alternative appraisal options, alternative methods for income and employment verification and the expanded use of power of attorney in loan closings.

FHFA also announced that Fannie Mae and Freddie Mac borrowers in a COVID-19 forbearance plan as of Feb. 28 will be eligible for an additional forbearance extension of up to three months. COVID-19 Payment Deferrals may now cover up to 15 months of missed mortgage payments. “To keep families in their home during the pandemic, FHFA is allowing borrowers to be in COVID-19 forbearance for up to 15 months and extending the Enterprises' foreclosure and eviction extension," said FHFA Director Mark Calabria.

The moratorium on single-family foreclosures of Fannie Mae and Freddie Mac borrowers and evictions of residents of real estate owned properties was also extended from its previous expiration of Feb. 28 to March 31.

|

|

|

|

CFPB will prioritize consumer complaints

Acting Consumer Financial Protection Bureau (CFPB) Director Dave Uejio directed the Division of Consumer Education and External Affairs (CEEA) to ensure consumer experiences are at the center of CFPB policymaking. “Moving forward CEEA should redouble its efforts to ensure the bureau engages all consumers who are economically suffering,” said Acting Director Uejio. This engagement includes prioritizing consumer complaints, which are at an all-time high, according to the agency.

Acting Director Uejio suggests that certain regulated entities have been “lax” in their treatment of consumer complaints and have failed to meet the CFPB’s expectation that companies will respond to those complaints in a substantive and timely manner. “I also understand that consumer advocates have found disparities in some companies’ responses to Black, Brown, and Indigenous communities,” said Acting Director Uejio. “This is unacceptable.” CFPB’s consumer response division will prepare and publish a report on those companies with a “poor track record” on complaint responsiveness.

|

|

|

|

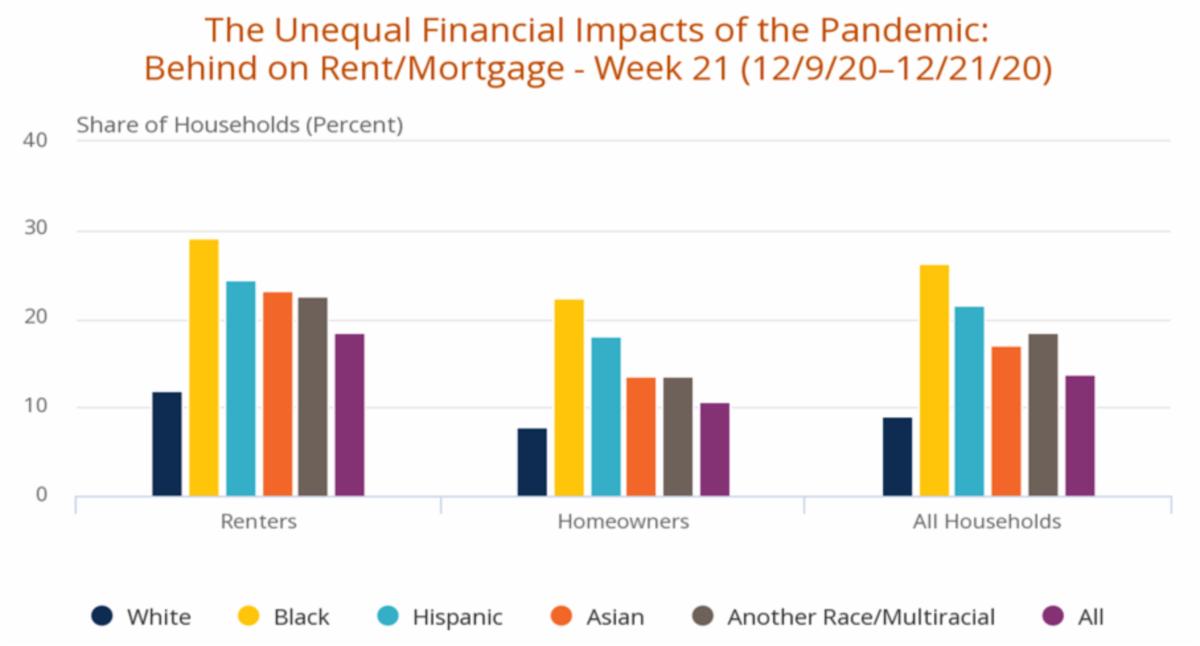

Chart of the week: COVID-19 continues to have a disparate impact on minority households

Harvard’s Joint Center for Housing Studies updated its interactive tool to assess the economic impacts of the pandemic with new data from the Census Bureau’s Household Pulse Survey. The analysis reveals that the disparate impact of the pandemic on minority households has worsened for both renters and homeowners.

|

|

As more renters fall behind on rent, utilities and other household bills, “the most desperate are already improvising by moving into even more crowded homes, pairing up with friends and relatives, or taking in subtenants,” according to a recent New York Times article. “Such changes are not directly reflected in rent rolls or credit card bills, but various studies show that disrupted and overcrowded households have a host of knock-on effects, including poorer long-term health and a decline in educational attainment.”

JPMorgan Chase convened industry leaders to discuss the impact of COVID-19 on affordable housing. Linda Mandolini, president at Eden Housing; Robert Morse, partner and executive chairman at Bridge Investment Group; Brenda Rosen, president and CEO at Breaking Ground; and Joe Weatherly, senior vice president of development at McCormack Baron Salazar discussed how their organizations have managed COVID-positive tenants, attracted new donors, addressed food insecurity and managed the continuously high demand for the scarce inventory of affordable housing units.

|

|

Monday, February 15

Tuesday, February 16

Wednesday, February 17

Thursday, February 18

Friday, February 19

|

|

The National Housing Conference has been defending the American Home since 1931. We believe everyone in America should have equal opportunity to live in a quality, affordable home in a thriving community. NHC convenes and collaborates with our diverse membership and the broader housing and community development sectors to advance our policy, research and communications initiatives to effect positive change at the federal, state and local levels. Politically diverse and nonpartisan, NHC is a 501(c)3 nonprofit organization. |

|

Defending our American Home since 1931 |

|

Copyright © 2021. All Rights Reserved. |

|

|

|

|

|

|